Bond Jitters, Oil Myths, and Fed Drama—Where Smart Capital Should Really Look

📈 A Shaky Start for Global Assets Markets have entered September in a state of restless calm —steady on the surface, jittery underneath. Between bond market sell-off fears, oil price forecast chatter, and political pressure on the Federal Reserve , investors have had no…

📈 A Shaky Start for Global Assets

Markets have entered September in a state of restless calm—steady on the surface, jittery underneath. Between bond market sell-off fears, oil price forecast chatter, and political pressure on the Federal Reserve, investors have had no shortage of signals to interpret. What’s striking is how easily headlines can mislead: whispers of Brent crude oil price soaring proved hollow, while U.S. Treasury yields and U.K. gilt yields quietly spiked to levels not seen in decades. This isn’t a moment for unquestioning optimism or panic selling—it’s a moment for careful reading of the fine print. And sometimes, the fine print is louder than the headlines.

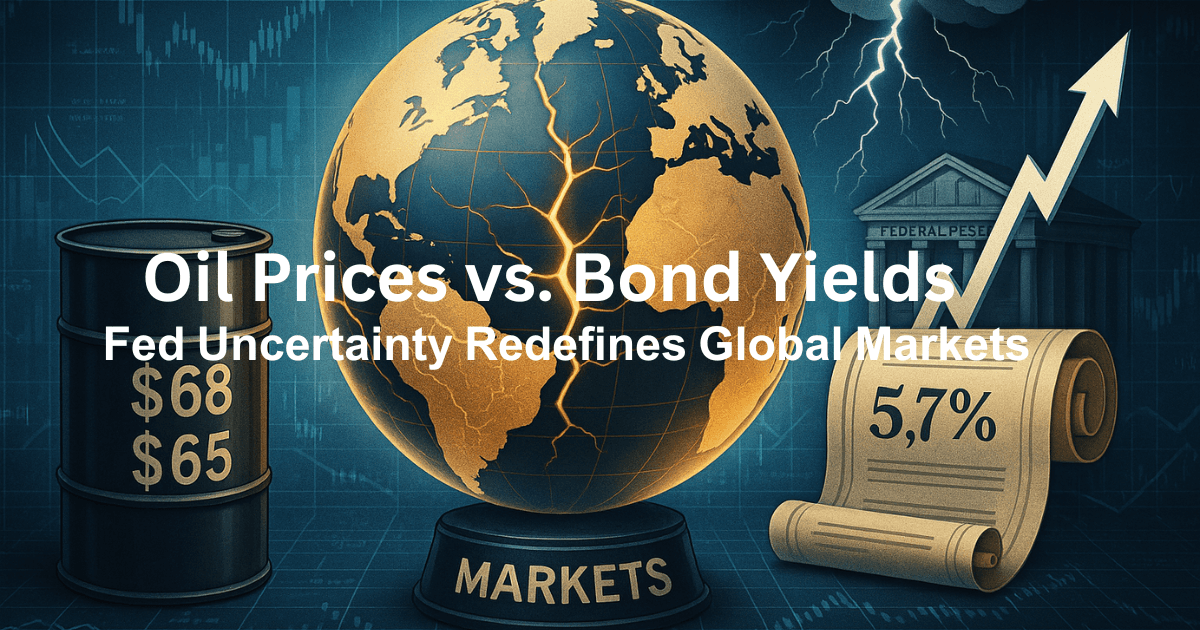

🛢️ Oil Prices: High Talk, Low Reality

Despite buzz around “nine-month highs,” the real story was more modest. The WTI crude price today hovered closer to $65, while the Brent crude oil price settled near $68—a far cry from the imagined $90 threshold. Supply worries stemming from Russia–Ukraine disruptions initially provided early support, but sentiment shifted as traders braced for the next oil price forecast update from OPEC+. The EIA’s outlook projects Brent drifting below $60 by year-end as inventories rise and demand cools. It’s a sobering reminder that even bullish energy bets can be short-lived. Capital Cue: The oil narrative remains a trader’s market—ripe for quick plays, but not the long-term growth story that some headlines pitch.

⚡ Volatility Without Fireworks: Data and the Fed

Investors focused on market volatility drivers tied to economic data, including the impact of Non-Farm Payrolls, JOLTS figures, and the ISM Services PMI. The PMI landed at 55—expansionary—but the employment index slumped to 46.5, flashing contraction. That mix—demand holding but labor weakening—fed speculation about rate cuts. Meanwhile, the debate over Fed independence escalated as political noise began to infiltrate the discussion. Yields dipped after spiking early in the week, showing how quickly narratives can flip. Tactical Insight: Expect whipsaw action. Not crisis-level swings, but just enough chop to reward those hedging against surprise outcomes.

💰 Silvercrest’s Calm Lens on Valuations

Silvercrest, in its valuations outlook, noted that elevated investment valuations don’t necessarily mean a “bubble.” Instead, they argued that low volatility provides room for rebalancing or hedging strategies. Their tone was calm: elevated, yes; dangerous, no. For long-term allocators, that matters more than daily noise. Investor Radar: This is a season for rotation, not retreat. Trim the high flyers, boost quality defenses, and prepare for shifting cycles.

🇬🇧 U.K. Households Find Relief, Banks Go Digital

Beyond global macro stress, the U.K. delivered some real relief for families. From September, households in the UK can gain up to £7,500 in childcare savings, thanks to expanded 30-hour free childcare benefits. It’s a direct boost to disposable income, which may support consumption. At the same time, high-street banks are closing branches and ending paper statements. Digital strategies dominate, but they highlight a deeper concern about fiscal sustainability for banking models under pressure from wage and inflation. Smart Capital Signal: Families benefit from the policy tailwind, but banks are still searching for margin resilience in a digitized future.

🏦 Stocks Sink, Bonds Rally—and the Fed Takes the Stage

The Fed independence debate intensified after Donald Trump attempted to remove Governor Lisa Cook. Over 600 economists publicly backed Cook, while markets grew uneasy. U.S. equities slipped as U.S. Treasury yields and other global bond yields experienced significant fluctuations, with political risk, rather than economic logic, dominating sentiment. Portfolio Pointer: Bonds reclaimed their role as a shock absorber in portfolios, even with higher yields. Stocks, meanwhile, struggled under the weight of political gamesmanship.

🌍 Bond Market Rout: Debt Sustainability Under Fire

Perhaps the most structural story came from sovereign debt. U.K. gilt yields soared to 5.7%, their highest in 27 years. France and Germany faced similar moves, while global bond yields and U.S. Treasury yields surged due to concerns about deficits. The culprit? Budget deficits, weak demand from traditional buyers, and tariff uncertainties. It was the kind of bond market sell-off that signals more than just noise—it speaks to long-term concerns about fiscal sustainability. Strategic Compass: High yields may tempt bargain hunters, but fiscal arithmetic is unforgiving. Waiting for true capitulation might be smarter than chasing a “cheap” entry now.

🥂 Closing Thoughts: Reading Between the Rattles

The message for investors is subtle but clear. The oil price forecast doesn’t point to a new boom—it points to softer demand. Investment valuations that are elevated don’t scream 'bubble'—they hint at selective opportunity. And global bond yields aren’t just volatile—they’re warning of deeper fiscal strain. Noise will always be loudest. But investors who read the details—the PMI employment index, the childcare relief data, the Silvercrest analysis—see a more measured picture. This is a market rattling its pots, not yet boiling over. Smart positioning matters more than headline-chasing.

Sources

- Reuters – Oil settles higher on weaker dollar, supply worries

- Reuters – Oil prices dip on OPEC+ output talk

- U.S. EIA – Short-Term Energy Outlook

- NAGA – Top Economic Events September 2025

- Fidelity – ISM Services PMI August 2025

- Silvercrest Group – Economic Review September 2025

- WiredGov – UK Childcare Rollout

- Yahoo UK – Free childcare extended

- Reuters – Fed independence debate

- MarketWatch – Global bond rout

- Barron’s – Bond market fears

Market Munchies and Mode Mobile communications are for informational purposes only, and are not a recommendation, solicitation, or research report relating to any investment strategy, security, or digital asset. All investments involve risk including the loss of principal and past performance does not guarantee future results.

Any information contained in this commentary does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no guarantee that any statements or opinions provided herein will prove to be correct.