Light Trading, Heavy Meaning: What Quiet Holiday Markets Reveal About 2026

The final trading week of 2025 offered little in the way of volume or volatility—but that does not mean it lacked significance. Holiday-thinned markets often reveal positioning rather than performance, and this year’s transition into 2026 provided a clear look at how investors…

The final trading week of 2025 offered little in the way of volume or volatility—but that does not mean it lacked significance. Holiday-thinned markets often reveal positioning rather than performance, and this year’s transition into 2026 provided a clear look at how investors are preparing for the months ahead.

Equities softened modestly, financials recalibrated expectations, gold finished the year strong, artificial intelligence spending shifted toward infrastructure, and crypto markets stabilized without speculative excess. Rather than signaling risk aversion, the week reflected consolidation after a powerful year—and a recalibration of assumptions heading into 2026.

U.S. Equities: Pausing, Not Breaking

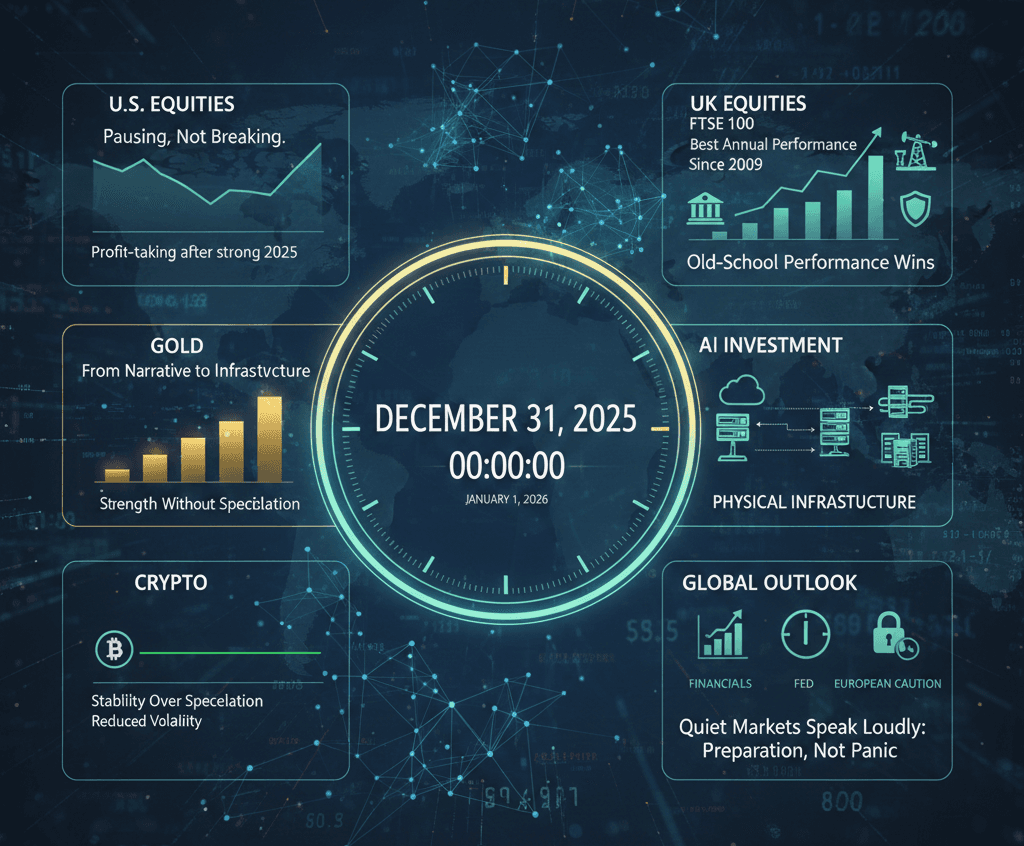

U.S. stocks edged lower during the final days of December, driven primarily by profit-taking in technology after a strong 2025. The move lacked the hallmarks of stress. There was no spike in volatility, no broad-based risk-off behavior, and no deterioration in market breadth.

Instead, investors appeared to be trimming exposure, locking in gains, and waiting for January’s return of liquidity and capital flows. Historically, late-December weakness following strong annual returns has often reflected positioning rather than a change in trend.

Market implication: The pullback reflects digestion after an outsized year, not a reversal of the broader equity narrative.

UK Equities: Old-School Performance Wins Again

While global markets focused on growth and technology narratives, the UK quietly delivered one of its strongest years in over a decade. The FTSE 100 finished 2025 with its best annual performance since 2009, driven by banks, energy companies, and defensive sectors.

Cash flow generation, dividend income, and valuation discipline once again proved effective in a higher-rate, late-cycle environment. The UK market’s performance reinforced a broader global theme: in periods of macro uncertainty, durability can outperform excitement.

Macro takeaway: Markets emphasizing income, balance sheets, and pricing power continue to attract capital in tight financial conditions.

The Fed: Quiet Data, Clear Caution

With most economic releases sidelined during the holidays, attention shifted to the Federal Reserve’s December meeting minutes. Policymakers reiterated a cautious stance: rate cuts remain likely in 2026, but inflation risks have not been fully neutralized.

The tone suggested patience rather than urgency. While easing is expected, it is unlikely to arrive at a pace that dramatically loosens financial conditions in the near term.

Policy signal: The Fed is preparing to ease—but remains highly data-dependent, with no appetite for premature acceleration.

Financials: Yield Curve Reality Sets In

Bank stocks weakened slightly as expectations for rapid rate cuts faded. The yield curve remains stubbornly flat to inverted, limiting optimism around net interest margin expansion.

Without a clearer steepening of the curve, financial stocks face near-term pressure, particularly after outperforming earlier in the cycle on policy pivot hopes.

Sector read: Financials remain sensitive to curve dynamics, not just headline rate moves.

Europe: Caution Remains the Operating Principle

Sweden’s central bank held rates steady, echoing the broader European stance. While inflation has eased across the region, policymakers remain wary of declaring victory too early.

Across Europe, the prevailing posture is restraint. Central banks are willing to wait for confirmation that inflation is firmly under control before shifting decisively.

Central bank outlook: The easing cycle is likely to be slow and uneven, reinforcing regional divergence.

Gold: Strength Without Speculation

Gold closed 2025 with strong gains, supported by sustained central bank purchases, geopolitical uncertainty, and late-cycle hedging behavior. Importantly, the move lacked speculative excess—there was no surge in retail-driven momentum or volatility.

That calm strength often reflects institutional positioning rather than fear-driven demand.

Hedging insight: Gold’s performance suggests preparation, not panic.

AI Investment: From Narrative to Infrastructure

One of the clearest signals of the week came from artificial intelligence capital flows. SoftBank’s infrastructure-focused acquisition highlighted a shift underway: AI investment is moving from conceptual growth stories to physical buildout.

Data centers, power supply, cooling systems, fiber networks, and hardware capacity are now central to the AI expansion. The next phase of growth is increasingly capital-intensive rather than purely software-driven.

Capital trend: The AI cycle is entering its industrial phase, favoring infrastructure and real assets.

Technology Outlook: CES Sets the Tone

With CES 2026 approaching, attention is turning to the next wave of technology narratives. Artificial intelligence integration across hardware, robotics, and consumer devices is expected to dominate early-year headlines.

Historically, January has played a key role in shaping which technology themes persist and which fade. Initial enthusiasm often gives way to more selective adoption by February.

Tech takeaway: Early-year narratives matter—but execution will determine staying power.

Crypto: Stability Over Speculation

Despite political and corporate token headlines, crypto markets remained relatively stable. Bitcoin held firm through the holiday period, supported by ETF-related flows and early-year positioning.

The absence of excessive leverage or speculative mania stands in contrast to prior cycles and may signal a maturing market structure.

Crypto signal: Reduced volatility and stronger base support suggest a healthier setup than past holiday periods.

The Bigger Picture: Quiet Weeks Speak Loudly

Holiday markets tend to strip away noise. With fewer participants and less liquidity, the actions that remain often reflect conviction rather than momentum.

This week showed:

- Technology consolidating without stress

- Gold attracting steady institutional demand

- AI capital flowing into physical infrastructure

- Crypto maintaining structure rather than spectacle

These are not signs of complacency. They are signals of preparation.

Looking Ahead to January

As liquidity returns and earnings season approaches, markets will test these early signals. ISM data, bank lending trends, Fed commentary, and post-CES corporate guidance will begin shaping expectations for the first quarter.

The calm at year-end was not indecision—it was positioning.

Bottom line: Quiet markets don’t perform; they reveal. And what they revealed at the start of 2026 was restraint, discipline, and selective confidence rather than fear or excess.

Sources:

- https://seekingalpha.com/article/4854222-umh-properties-undervalued-growth-in-a-high-demand-sector

- https://seekingalpha.com/article/4853708-d-wave-quantum-is-looking-like-the-early-quantum-computing-winner-upgrade

- https://www.barrons.com/livecoverage/stock-market-news-today-121825/card/tech-stock-futures-rise-as-markets-weigh-up-ai-and-inflation-9VG7bmuOSekoWcID6LLF

- https://www.barrons.com/livecoverage/stock-market-news-today-121825/card/u-s-treasury-yields-decline-cpi-data-unlikely-to-be-a-game-changer--tkWZbZVIhXbehGCNLQlP

- https://www.reuters.com/world/americas/trump-orders-blockade-sanctioned-oil-tankers-leaving-entering-venezuela-2025-12-16/

Market Munchies and Mode Mobile communications are for informational purposes only, and are not a recommendation, solicitation, or research report relating to any investment strategy, security, or digital asset. All investments involve risk including the loss of principal and past performance does not guarantee future results.

Any information contained in this commentary does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no guarantee that any statements or opinions provided herein will prove to be correct.