Markets Digest a Week of AI, Macro Signals, and Geopolitical Tension

After a week of thin, holiday-influenced trading, markets revealed where investors are willing to commit capital—and what is currently being sidelined. With fewer distractions, the underlying trends in technology, banking, energy, and macro policy became clearer. Geopolitical…

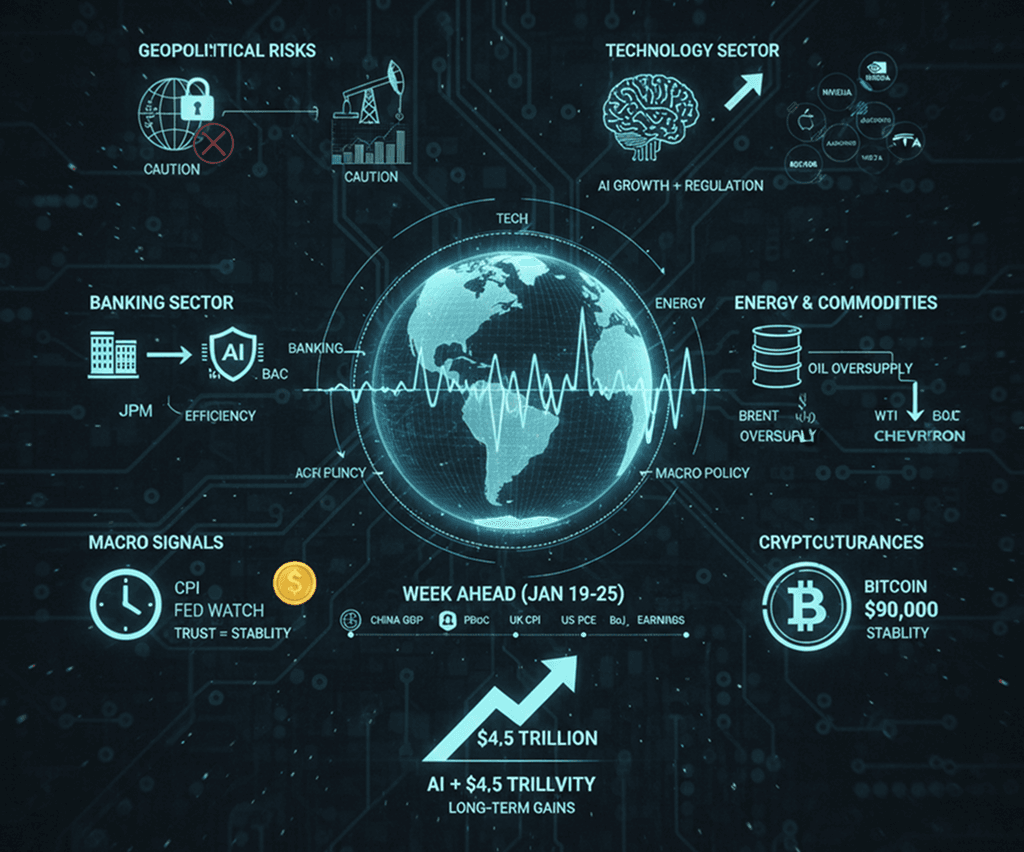

After a week of thin, holiday-influenced trading, markets revealed where investors are willing to commit capital—and what is currently being sidelined. With fewer distractions, the underlying trends in technology, banking, energy, and macro policy became clearer.

Geopolitical Risks Remain in Focus

Trade disputes, sanctions, and power-politics developments continued to shape investor behavior. While there were no sudden shocks, the market remained attentive to global events, evaluating risk and pricing exposure accordingly.

- Market impact: Investors maintained caution in sectors sensitive to international policy, particularly energy.

Technology Sector: Growth Meets Scrutiny

Tech stocks, particularly in AI and semiconductors, continued to garner attention but at a more measured pace. Export controls and regulatory oversight have introduced new considerations, prompting investors to recalibrate expectations.

- NVIDIA (NVDA): $187.38 (+1.2%) — TSMC’s positive outlook reassured investors on AI chip demand, supporting moderate gains.

- Apple (AAPL): $259.93 (−0.6%) — A quiet week for Cupertino after recent gains, with investors digesting prior performance.

- Alphabet (GOOGL): $332.62 (−0.4%) — Following a $4 trillion market-cap milestone, the stock moderated as traders took profits.

- Meta Platforms (META): $612.80 (+0.9%) — Focused on efficiency in AI investments, maintaining steady margins.

- Tesla (TSLA): $443.74 (+1.5%) — Broad market support lifted the stock, though autonomous vehicle chatter remains muted.

Takeaway: AI remains the primary driver of growth, but regulation and valuation considerations are tempering enthusiasm.

Banking Sector: Discipline and AI Investment

JPMorgan Chase and Bank of America demonstrated cautious optimism, balancing earnings momentum with measured AI investment strategies.

- JPMorgan (JPM): $312.07 (−0.3%) — Continued AI spending, though regulatory scrutiny tempers exuberance.

- Bank of America (BAC): $52.81 (+0.5%) — Solid earnings support steady gains, reflecting gradual recovery in financials.

Takeaway: Banks are emphasizing efficiency and strategic technology adoption rather than aggressive expansion.

Energy and Commodities: Oversupply Dampens Prices

Oil markets remained subdued despite geopolitical concerns. Ample supply continues to constrain prices.

- Chevron (CVX): $166.53 (−0.8%) — Softening oil prices trimmed optimism.

- Oil prices: Brent and WTI remained under pressure amid signals of reduced geopolitical risk.

Takeaway: Energy prices reflect supply abundance rather than immediate geopolitical shocks.

Macro Signals: Inflation, Growth, and Central Bank Watch

With the holiday period over, core macro data returned to focus. CPI, GDP, and rate expectations were closely monitored, with market participants emphasizing the quality of incoming data over narrative-driven sentiment.

- Federal Reserve scrutiny: DOJ probes regarding Chair Powell briefly rattled confidence, softening the dollar and supporting gold.

- Macro takeaway: Trust in central bank independence remains a critical invisible factor affecting market stability.

AI as a Productivity Accelerator

Recent estimates suggest AI could contribute up to $4.5 trillion in economic productivity gains over the coming years. Markets are increasingly assessing which firms and sectors will capture these benefits.

Takeaway: Long-term AI winners are expected to see structural gains in productivity, data infrastructure, and capital efficiency.

Cryptocurrencies: Stability Returns

Bitcoin consolidated near $90,000, demonstrating orderly market behavior and reduced volatility. Crypto markets showed signs of maturation, with leverage and flows remaining contained.

Takeaway: Calm behavior in crypto can indicate underlying structural strength.

Week Ahead: Key Dates and Data

January 19–25, 2026 brings several market-moving events:

- China Q4 GDP, industrial output, and retail sales — Signals for EM risk and commodity demand.

- PBoC policy update — Subtle liquidity or rate changes could influence global markets.

- UK CPI — Tests inflation persistence and BoE rate expectations.

- US PCE and growth indicators — Critical for Fed policy and rate-cut speculation.

- BOJ policy decision — Yen movements may impact global FX and liquidity.

- Earnings acceleration — Banks, financials, and early tech earnings will provide guidance clarity.

- Davos gatherings — Policy tone and global economic sentiment set by leaders and central bankers.

Week in Review: Market Highlights

- Tech and semiconductors led equity performance, supported by AI demand and strong TSMC results.

- Banks remained steady, balancing earnings optimism with regulatory considerations.

- Energy cooled as oversupply tempered enthusiasm despite geopolitical concerns.

- Crypto maintained a steady course, showing signs of market maturation.

- Macro data and central-bank scrutiny subtly guided investor expectations.

Conclusion: Thin holiday trading allowed markets to clarify what investors are prioritizing: AI growth potential, disciplined banking, structural productivity gains, and measured responses to macro and geopolitical developments. While not flashy, the week provided insight into durable trends shaping equity and commodity allocations.

Sources:

- NVIDIA / TSMC outlook – Reuters

- Wall Street / Tech rebound & oil easing – Reuters

- Wall Street steadies / Big Tech bounce / oil prices – AP NewsStock Market Today: Dow, S&P 500, Alphabet $4T milestone – Investors.com

- Dollar drops as DOJ subpoenas Powell – Reuters

- Powell DOJ subpoenas confirmation – AP News

- Top Senate Republican comments on Powell probe – Reuters

- Oil prices / Iran supply concerns – Reuters

- Oil price forecast / oversupply – Reuters

- Weekly Economic Calendar Jan 19–25, 2026 – LiteFinance

- TSMC Q4 revenue jump / beat forecasts – Reuters

Market Munchies and Mode Mobile communications are for informational purposes only, and are not a recommendation, solicitation, or research report relating to any investment strategy, security, or digital asset. All investments involve risk including the loss of principal and past performance does not guarantee future results.

Any information contained in this commentary does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no guarantee that any statements or opinions provided herein will prove to be correct.